Good news for savers as banks hike deposit rate

Banks in Bangladesh are raising the interest rate on deposits to pull funds with a view to tackling the liquidity shortage and meeting a higher demand for loans.

It comes as good news for savers, who saw the real return on their deposits turn negative as the interest rate continues to remain below the inflation rate.

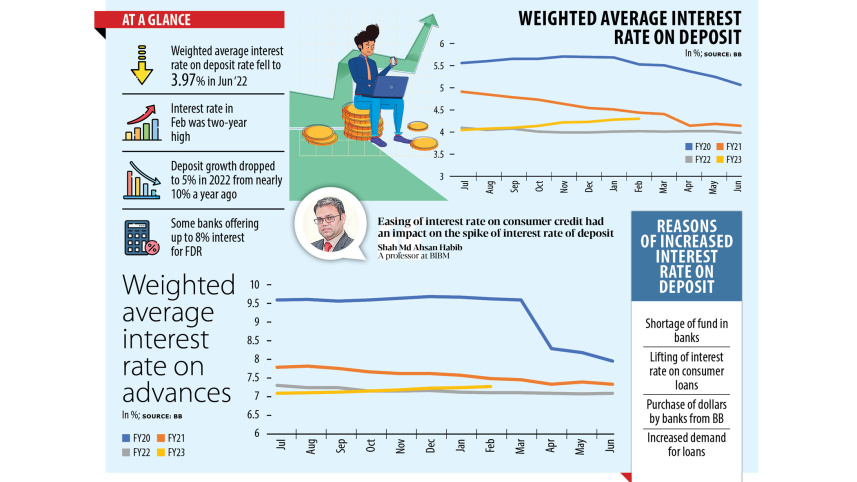

Data from the Bangladesh Bank showed that banks in February offered as high as 8 per cent for fixed deposits to attract savers, particularly from public institutions.

The weighted average interest rate on deposits stood at 4.31 per cent in February, the highest in nearly two years. In January, it was 4.29 per cent.

It fell to 3.97 per cent in June last year from a peak of 5.71 per cent recorded in November 2019.

The upward trend of the deposit rate comes at a time when banks are suffering from a liquidity shortage resulting from multiple factors, including the purchase of US dollars from the central bank in exchange for the taka to facilitate imports, withdrawal of funds by a section of savers amid allegation of irregularities in some Islamic banks, and a lack of propensity to save as inflation has exceeded the deposit rate for nearly a year.

Banks attracted 5 per cent higher deposits at Tk 15,88,010 crore in 2022. It was Tk 15,12,472 crore a year ago. In 2021, the overall deposit growth was nearly 10 per cent, according to central bank data.

Amid the slowing deposit growth and the fund shortage, a number of banks were compelled to become aggressive and they have been offering a higher rate on deposits over the last several months, said bankers.

The easing of an interest rate cap on consumer loans by the BB gave leeway to banks to raise the deposit rate.

In January, the central bank relaxed the lending rate cap for consumer loans, allowing banks to charge up to 12 per cent in interest rates on such credit products from 9 per cent, a rate that was maintained since April 2020.

"Most banks have already increased their interest rates on both loans and deposits slightly following the relaxations of interest rate cap, particularly for consumer loans, and the complete removal of the deposit floor rate by the central bank in its latest monetary policy statement," said Adil Chowdhury, president and managing director of Bank Asia Ltd.

BB data showed that the weighted average interest rate on loans edged up gradually. It reached 7.27 per cent in February, up from 7.24 per cent in January.

In July last year, the weighted average interest rate on advances was 7.09 per cent.

Syed Mahbubur Rahman, managing director of Mutual Trust Bank, says some banks face an asset-liability mismatch in the wake of a spike in forced loans after some clients failed to make payments against letters of credit on maturity.

"Besides, banks have bought foreign currencies from the central bank in exchange for a good amount of the taka to clear import bills."

The central bank injected around $9.50 billion into the banking sector between July 1 and February 9. A record $7.62 billion was supplied during the entire financial year of 2021-22 after import bills rocketed owing to escalated prices of commodities in the global markets.

"A lot of money has gone into the vault of the Bangladesh Bank from us as we have had to purchase foreign currencies," said Md Abdus Salam Azad, managing director of state-run Janata Bank, adding that the demand for loans from industries has picked up as well.

"Deposits are under stress. That's why banks have become aggressive in collecting deposits," said MTB's Rahman.

In Bangladesh, the real interest rate has become negative as inflation is much higher than the rates banks are offering to savers.

In March, consumer prices jumped to a seven-month high of 9.33 per cent following 8.78 per cent in February.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Inflation averaged 8.39 per cent last month from 8.14 per cent in February, way higher than the maximum deposit rate offered by some banks.

"If the real interest rate remains negative, many people will look for alternative investment opportunities. We already see property prices are going up," Rahman said.

Owing to a lower return on deposits against persistently higher inflation, Rifat Jahan, a homemaker in the capital's Mirpur, pulled funds from a private commercial bank last year and redirected the money into the stock market although the latter itself has been witnessing a bearish trend for months.

"A good amount of money will remain outside the banking system until we raise the interest rate on deposits to match it with the inflation rate. We also need to win back the confidence of customers and reassure them that money kept with banks is safe," Rahman said.

Bank Asia President Chowdhury hopes the easing of the lending rate cap, the complete removal of the deposit floor rate, and the upcoming market-based lending rate will create a positive impact on good borrowers and also for depositors to manage inflationary pressures.

Mohammad Ali, managing director of Pubali Bank, said the requirement for funds has increased among banks and it is fueling the interest rate.

"Many borrowers who in the past did not seek full disbursement of credits against their limits are now making the most of the ceiling. We see an increased utilisation of limits."

He, however, acknowledges that because of the spike in the interest rate on deposits, the cost of doing business for borrowers may go up.

"In some cases, banks' operating profits may fall."

Shah Md Ahsan Habib, a professor at the Bangladesh Institute of Bank Management, said the easing of the interest rate ceiling on consumer credits has pushed up the deposit rate.

"This is because banks were confronting fund challenges."

A mid-level official of a private commercial bank in Chittagong says some banks are even offering more than 8 per cent interest rate on longer-term deposit schemes.

"We are giving up to 7.75 per cent deposit rate on some schemes," he said, adding that his bank started to revise the deposit rates upwards in the first week of March.

Comments