Fix the accountability gap in the NBFI sector

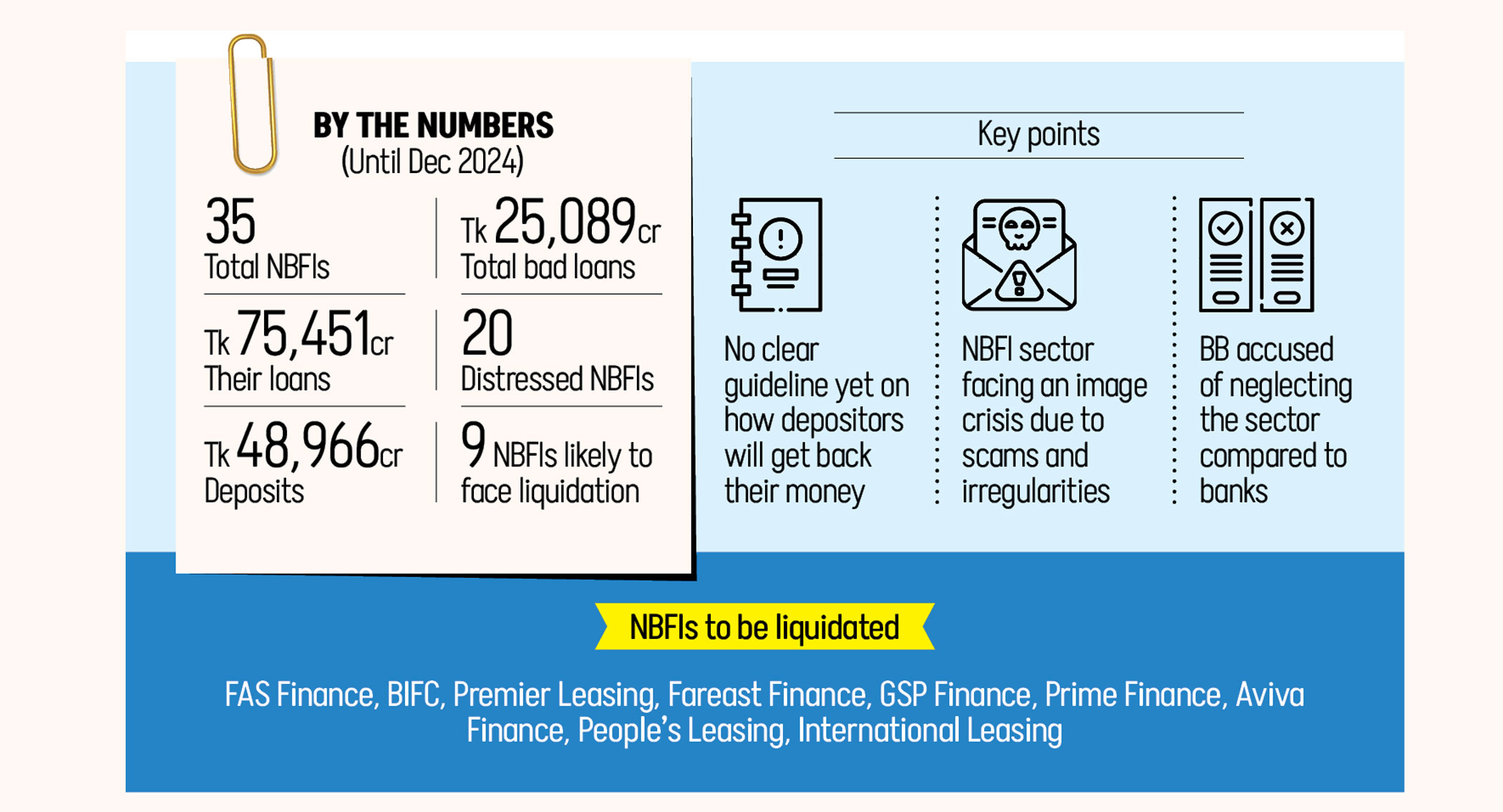

Trust is the only commodity a financial system truly sells. Interest rates and contract terms are secondary; what depositors ultimately buy is the belief that their savings are protected. Over the years, as six non-bank financial institutions (NBFIs) in the country has drifted towards insolvency on the watch of an inattentive regulator, that trust has been broken. And now, nearly 2,000 families are paying for a promise that was never kept. The six institutions, including FAS Finance, People's Leasing, Premier Leasing and International Leasing, collapsed due to mismanagement, governance failures, and bad loans. The Bangladesh Bank ordered them into liquidation in January. What’s striking is how long the regulator took to act, and how little has been done since to protect those depositors.

The NBFI sector occupies a peculiar blind spot in our financial system. When banks wobbled, the central bank moved, albeit belatedly and imperfectly. Deposit protection schemes, restructuring and public attention followed, but no equivalent efforts have been applied to the 35 NBFIs. Depositors were not making reckless bets; they simply parked funds in licensed entities that offered slightly higher returns. So the implicit contract was breached both by the institutions and by the regulator that licensed them.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. At a press conference on Wednesday, the affected depositors articulated a simple principle: a depositor is a depositor. It should not matter whether one’s savings sit in a bank or a leasing company. Both are licensed. Both issue receipts. Both attract ordinary people of ordinary means seeking ordinary security. We concur with the argument that leaving NBFI depositors exposed is not an acceptable practice.

The new BB governor has signalled that reform will continue, including pressing ahead with NBFI liquidation. That is the right instinct. Zombie institutions that cannot return deposits are better wound down than kept on life support. But liquidation without a credible deposit recovery mechanism is not reform. Instead, the authorities should act on three fronts. First, they must establish a time-bound repayment schedule. A three-to-six-month window—as the depositors' alliance has demanded—is not unreasonable for principal recovery, given the assets that remain to be liquidated. Second, deposit protection must be extended to NBFIs with appropriate calibration. Third, those responsible for the mismanagement and regulatory forbearance that enabled this crisis must face accountability.

There is an argument that bailing out NBFI depositors sets a moral hazard—that it is akin to rewarding those who chased higher yields. But the depositors in question were not hedge funds speculating on distressed debt. They were retired civil servants, charitable trusts funding orphanages, and families saving for medical emergencies. Moral hazard arguments carry weight when sophisticated actors take calculated risks.

Regulators are now attempting, with mixed results, to restore confidence in a financial system shaken by years of political interference and poor governance. Foreign investors are watching for signals. The handling of this NBFI crisis is, in miniature, a test of whether those signals are meaningful. The government therefore must remember that confidence is harder to rebuild than it is to squander, and nothing will restore confidence faster than ensuring those depositors are repaid.

Comments