Renting vs owning apartments: Key considerations for buyers

We humans have achieved some incredible things in our modern society. From launching rockets and robots into space and other celestial bodies, to liking cat videos from Norway instantaneously on our pocket computers, modern advancements sound like a utopia, if that is all you were projecting, of course.

We are also animals, however, by definition. And just like every other animal on the planet, we have certain core needs that must be fulfilled. Food, water, and air have been mostly met, the quality of which may be up for debate, but our shelter situation is a little murkier. For one thing, we are the only ones on the planet who pay to find shelter. But on the plus side, we skip the caves and tree-tops for apartments overlooking, well, other houses, and ponds!

For all latest news, follow The Daily Star's Google News channel.

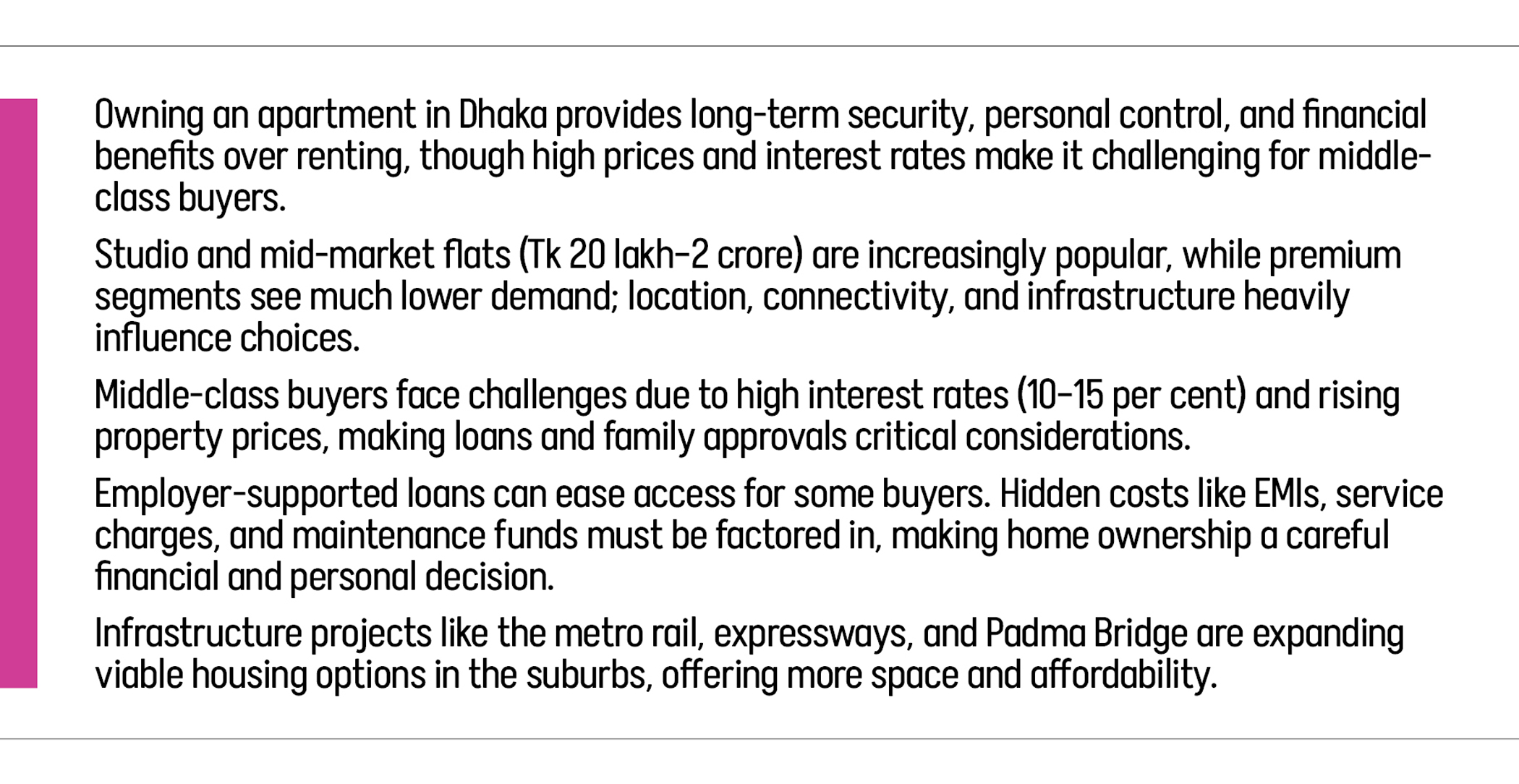

For all latest news, follow The Daily Star's Google News channel. Securing an apartment in Dhaka is a big step. It is much more than a simple financial transaction. For people navigating the busy life of the city, it is a key life milestone. This commitment is emotional. It is a long-term goal. It represents personal security, especially when you consider the fact that almost 80 per cent of Dhaka’s population still rent their homes.

From temporary spaces to a place that finally feels yours

Renting feels flexible, but you also get uncertainty. Your landlord can suddenly raise the rent or even sell the place. You do not fix big problems because the place is not yours. Owning changes this. You get control. You can update the kitchen, add a garden, anything!

Many first-time owners say they feel pure relief and joy when they get the keys. For Joyeeta and Tareq, a newly married couple, their first words after setting foot in their own apartment were “finally settled!”

Money is central to this choice, of course. Rent money is basically money out the window. But a home loan builds equity. The flat can gain value over time, especially since cities keep growing and land is scarce.

Studio apartments are now very popular as a way to start. They used to be for students or temporary living. Now, they are common for single people, young couples, and investors. The prices feel manageable. In good areas of Dhaka, a studio can cost Tk 30-80 lakh. If you look in Mirpur or Uttara, the price starts closer to Tk 20 lakh. Renting the same studio costs Tk 10,000 to Tk 40,000 each month. Do the maths, and owning suddenly starts to make sense.

“I have always dreamed of owning my own place. A place where I could live with my family,” states Moumita Ahmed, a Senior Officer at Sonali Bank PLC. “There was always a deep-seated desire in me to give my family the same sense of security and comfort in their old age that I was provided when I was growing up.”

However, reality hits different, and for a middle-class family, especially with the interest rates from 10 to 15 per cent per annum, and the kinds of prices for apartments, this kind of jump is difficult, if not impossible.

“Fortunately, my workplace provides its employees with the option of much lower interest, which has reignited my desire to go for my own home,” affirmed Moumita.

For those like Entekhab Hasan, owning a home is all about security. “With things like inflation, wage stagnation in many workplaces, and the ever-present concern of aiding ailing parents, money is always a dire concern. And on top of that, paying rent genuinely feels like throwing money away, because there is no return on this. If we were paying off a home loan, at least I knew that at the end of it all, we would get ownership. However, getting parents to agree is a tricky obstacle,” confessed Hasan.

Where the market is still moving

The overall pace of apartment sales has slowed sharply. Despite the drop, the property market has found an unlikely saviour in the middle tier. Developers now recognise that the mid-market segment is the sector’s main source of cash flow. It is the real lifeline for the entire industry.

Upper-middle-income families sustain this segment. They are professionals. They typically look for flats priced between Tk 1 crore and Tk 2 crore. These buyers remain active in the market. Demand in the premium segment has plunged by more than 60 per cent. That premium segment covers flats over 2,000 square feet and priced over Tk 2.5 crore.

Location is a key point to consider, and it also almost always shapes the choice.

Top areas like Gulshan, Banani, and Baridhara cost much more money. They also keep their value even when the market slumps. Areas further out, like Uttara, Bashundhara, and Purbachal, bring in buyers who swap high status for more space and newer infrastructures.

“Places like Dhanmondi, Gulshan, and Banani are simply out of reach for me, and maybe a lot of other people. So, I am looking at mostly places like Motijheel, Khilgaon, Malibagh, and especially Aftabnagar, as it has the potential to be the next big neighbourhood,” states Moumita Ahmed.

“My range is between Tk 1 crore, so I am looking mostly in the 1,200 sq ft range. However, the issue I am facing is that these areas have become pricey, somewhere around Tk 7,000-Tk 11000 per sq ft,” observed Ahmed.

The metro rail, as well as the expressway, has made Uttara very attractive. Apartments there sell for about Tk 12,000 per square foot. Bashundhara has planned communities, with prices from Tk 7,000 to 8,500 per square foot. Basila is even lower at Tk 5,000 to 6,000 per square foot. Good connections turn a distant suburb into a practical option.

New roads and bridges are opening up southern and northern routes. This is pulling potential owners out of crowded central Dhaka toward cheaper areas that have more open space. The Padma Bridge, for example, caused a housing boom along the Dhaka–Mawa–Bhanga expressway.

The hidden costs behind the dream

The greatest deterrent for people looking to buy is the financial pressure. Realtors confirm that stubborn bank loan rates are crippling purchasing power. These high rates often sit in the double digits. Current home loan interest rates typically range from 10.5 per cent to 13.5 per cent per annum. Some rates have reportedly hit 14 per cent or even 15 per cent.

These rates are exorbitant. They result in high Equated Monthly Instalments, or EMIs. High EMIs actively discourage potential buyers. This is especially true for those buyers sensitive to interest fluctuations. The lowest-end segment of buyers is also affected, as they are the most sensitive to these financial pressures.

The real cost of owning a home goes beyond the flat’s base price. This is what often catches buyers off guard. A successful purchase requires a comprehensive budget. You must account for these hidden costs.

Buyers must also budget for ongoing monthly service charges. These pay for the maintenance of common areas, security, and elevators. You also contribute to an advanced sinking fund for future major repairs.

Ultimately, the decision to be a homeowner comes down to your timing and readiness. Some wait for that perfect moment that, realistically, never arrives. While others take that step when they feel they are in a stable enough situation. Moving from renting to owning is kind of like claiming a piece of your future.

Dhaka is changing fast, and having your own place offers reliable stability. This is where you will make memories, perhaps raise children, and spend your retirement. The size of the space matters less than the feeling that it is permanent. Be it a modern studio downtown, or a big family flat at the city’s edge, those new keys open more than just a door. They open a chapter that finally feels like home.

Illustration: Intisab Shahriyar

Comments