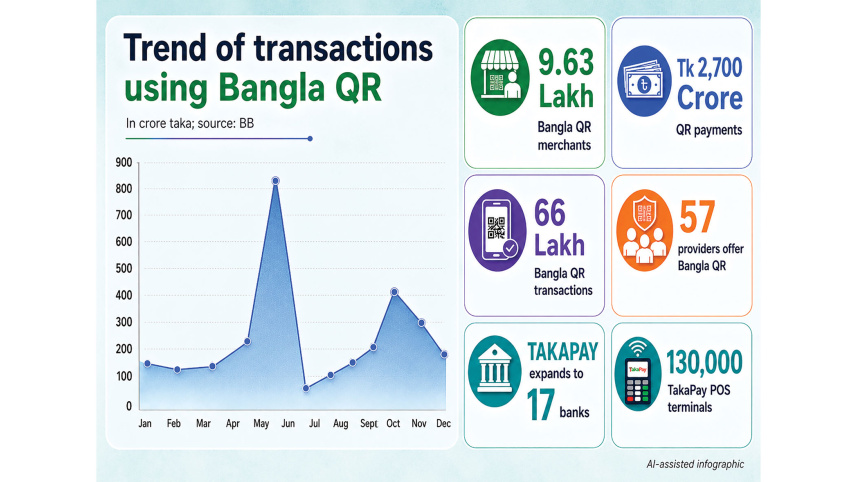

Bangla QR scales to 9.63 lakh merchants

Bangla QR, Bangladesh’s interoperable quick response (QR) payment collection system introduced by the central bank, expanded to nearly 9.63 lakh merchants by the end of 2025, reinforcing its role in the digital payments ecosystem.

A total of 46 banks, seven mobile financial service (MFS) providers, and four payment service providers (PSPs) now offer the service, according to the Payment Systems Report 2025, published by the Bangladesh Bank (BB) on Monday.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. More than Tk 2,700 crore worth of payments were processed through the system last year.

The latest data comes as the central bank seeks to use Bangla QR to achieve 80 percent digital transactions within the next decade and transform the country into a cashless, technologically empowered economy.

In April this year, the BB directed all banks, MFS providers, PSPs and payment system operators (PSOs) to replace proprietary QR codes at merchant points with Bangla QR by June 30, warning of penalties of up to Tk 30 lakh for non-compliance.

A total of 46 banks, seven mobile financial service providers and four payment service providers now offer the Bangla QR service

The central bank launched the interoperable QR-based settlement system in January 2023 to improve transparency, reduce risks, lower transaction costs and accelerate digital payments.

As part of its target of making 75 percent of transactions cashless by 2027, the authorities have already made QR payment facilities mandatory for obtaining or renewing trade licences nationwide.

The platform enables customers of participating banks and MFS providers to make payments using a single QR code, unlike proprietary systems that restrict transactions to specific providers.

According to the report, the payment network reached a major milestone in November last year when banks, PSPs, PSOs and MFS providers began conducting live interoperable transactions for the first time. The development allowed customers to transfer funds to any registered bank account, MFS or PSP wallet, regardless of the service used.

The central bank followed up on this on December 15, 2025, by approving instant settlement for Bangla QR transactions, a move aimed at improving liquidity for small traders.

BB data showed that nearly 66 lakh transactions were conducted through the payment system. However, Bangla QR still accounted for only a small share of transactions routed through the National Payment Switch Bangladesh (NPSB).

The report also showed that the total number of transactions across Bangladesh’s payment system rose 19 percent to 108 crore in 2025, although the overall value of transactions slipped 1 percent.

Alongside Bangla QR, the BB’s national debit card, TakaPay, also gained momentum in 2025. Introduced in November 2023 to reduce reliance on international card networks and lower transaction costs, TakaPay transitioned from magnetic-stripe cards to chip-based debit cards in June 2024, when nine banks first rolled them out. The report said 17 banks are now actively issuing TakaPay cards.

All TakaPay transactions are processed through the NPSB, giving cardholders’ access to around 16,500 ATMs and cash recycler machines, as well as approximately 130,000 point-of-sale terminals nationwide.

“This integration ensures seamless interoperability across participating banks, merchants, and ATMs, allowing cardholders to transact reliably regardless of their issuing institution. By consolidating transaction processing through a unified national switch, TakaPay eliminates fragmentation and establishes a cohesive foundation for digital payments,” the BB said.

The report said Bangladesh had 792,132 credit card users as of December 2025, making credit cards the smallest category of digital payment instruments, well behind the 82.3 lakh debit cardholders and 1.23 crore savings account holders.

The data highlighted a stark urban-rural divide. Cities accounted for 99.41 percent of credit card transaction volume and 92.69 percent of transaction value, leaving rural areas with just 0.59 percent of volume and 7.31 percent of value.

The BB attributed the disparity to structural barriers, including income documentation requirements, limited access to credit bureaus and merchant card-acceptance infrastructure that remains overwhelmingly concentrated in urban areas.

To narrow the gap, the central bank suggested expanding alternative digital credit models, such as transaction-based lending linked to mobile financial services usage, which could broaden access to credit without weakening risk controls.

Comments