Bangladesh economy caught in the crossfire

The economic shockwaves from the Iran war are rippling far beyond the Middle East. Heavily dependent on the Gulf for energy and sustained by remittances from the same region, Bangladesh remains particularly exposed, and a new World Bank assessment warns that this external shock could amplify our existing vulnerabilities, slowing growth, fuelling inflation, and pushing thousands back into poverty.

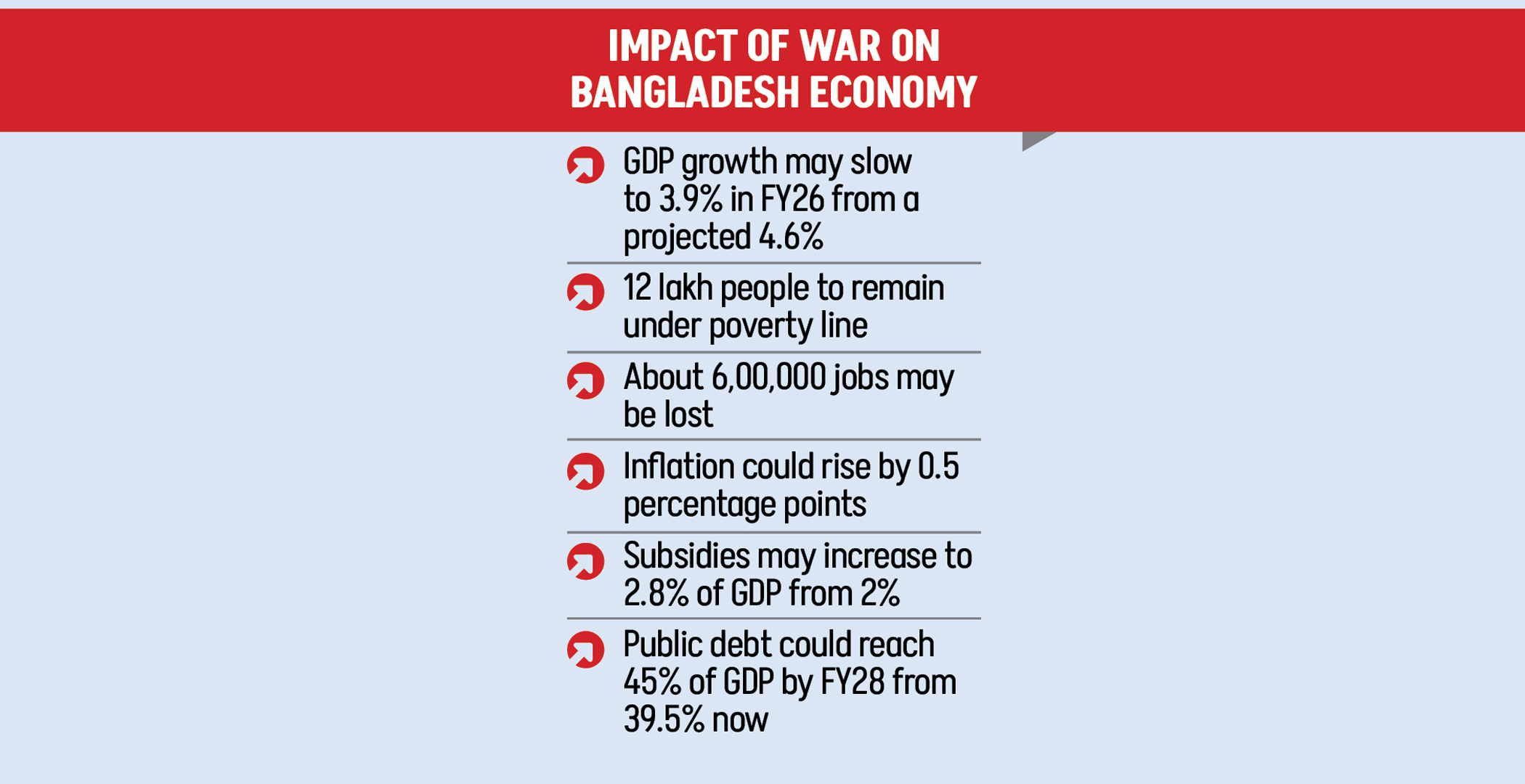

The growth outlook has already dimmed. Real GDP expansion, previously downgraded to 4.6 percent for the current fiscal year, is now projected to fall further to 3.9 percent. For an economy that needs momentum after three consecutive years of rising poverty, this is a serious setback. An estimated 12 lakh people who were expected to move out of poverty will now remain trapped, while about 600,000 jobs risk disappearing altogether.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Bangladesh imports 60-65 percent of its crude oil from the Gulf and also sources up to 75 percent of its LNG from the region, primarily Qatar. As energy prices climb, the import bill swells, widening the trade deficit and putting pressure on the taka. These costs ripple quickly through the economy, raising the price of transport, food production, and industrial output. Inflation, already elevated, is likely to gather further pace, hitting the poorest households hardest. At the same time, a second pressure point looms: remittances. Millions of Bangladeshi workers are now employed in economies that are themselves vulnerable to prolonged instability. If hiring slows or wages weaken, the impact will be felt directly in Bangladesh’s villages and towns. The flow of remittances could begin to thin.

What makes this moment more precarious is the condition of the domestic economy. Bangladesh is entering this external storm with structural weaknesses already exposed. The new government has inherited tight fiscal space, a fragile banking system, and persistently weak revenue mobilisation. These constraints leave little room to absorb additional shocks.

Higher global energy prices will inevitably deepen fiscal pressures. Subsidy requirements for power, gas, and fertiliser are set to rise sharply. If domestic prices are not adjusted, subsidy spending could climb to 2.8 percent of GDP in FY26 from 2 percent now, crowding out investment in health and education and forcing the government to depend more on borrowing. In an already constrained financing environment, that path is risky. Public debt, if left unchecked, is projected to exceed 45 percent of GDP by FY28.

The policy response, therefore, cannot be timid. The central bank must resist the temptation to rely on unsterilised money creation to prop up weak banks and instead maintain a firm monetary stance to contain inflation. At the same time, relief measures should be carefully targeted, reducing import duties on essential food items and expanding safety nets for the most vulnerable households. The authorities must also move on long-delayed reforms. Energy subsidies need to be gradually rationalised to ease fiscal pressure. Tax policy and administration must be overhauled to broaden the revenue base and reduce dependence on domestic borrowing. Without these steps, short-term firefighting will only deepen long-term fragility. If the government is to withstand the current turbulence and return to a path of inclusive growth, decisive reform is urgent.

Comments