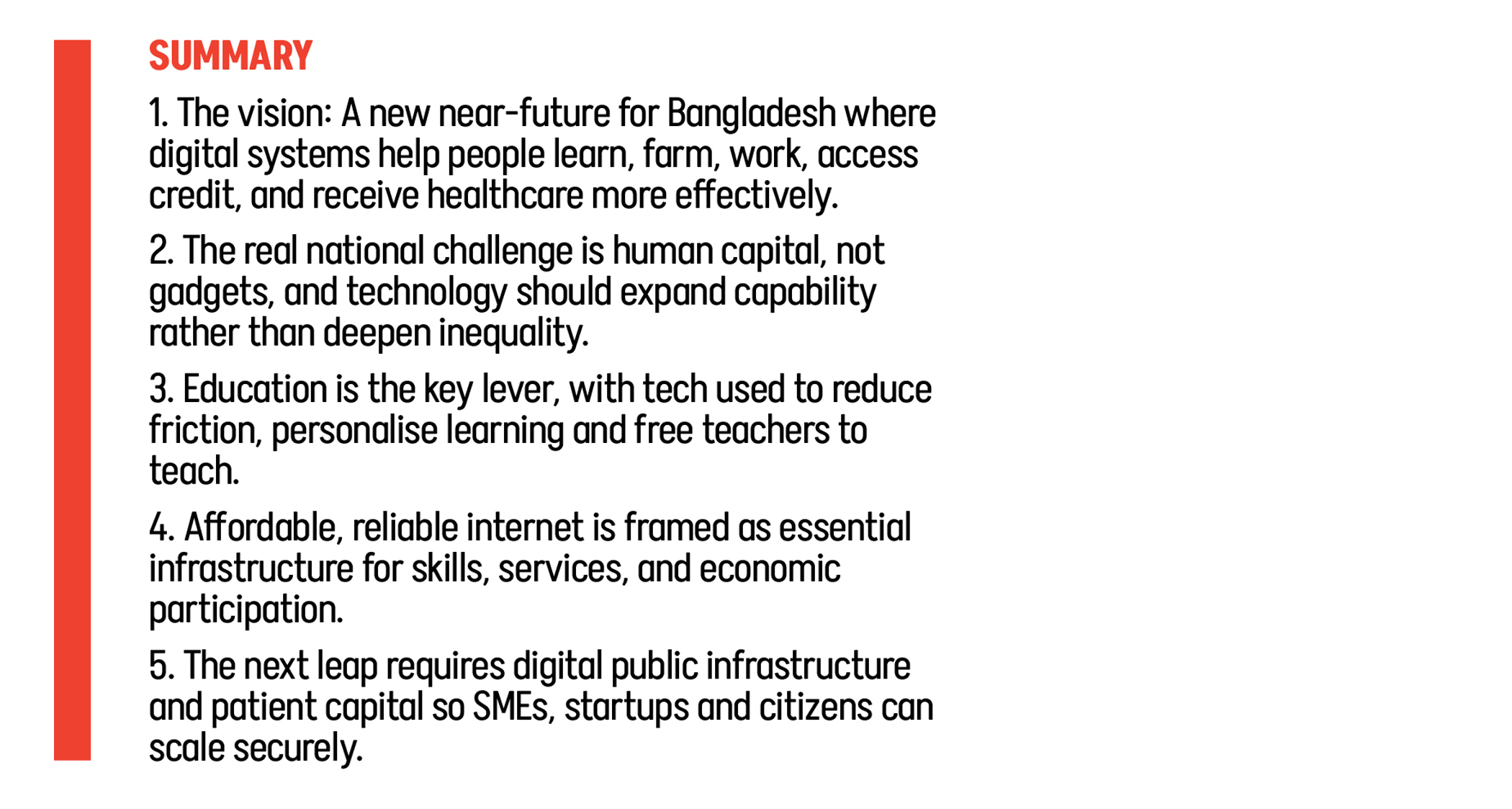

Building Bangladesh’s human capital in a digital age

Just before sunrise in 2030, a grade 8 student named Rafi sits at a wooden desk in a tin-roofed home outside Rangpur. His mother is boiling water for tea. The electricity has stayed on through the night. On the tablet in front of him, a mathematics lesson adjusts quietly as he works through it, slowing where he struggles and moving faster where he does not. His teacher will see the same data later that morning, not to rank him, but to understand him.

Several hundred kilometres south, a farmer in Patuakhali checks his phone before stepping into the field. The app tells him how much moisture remains in the soil, which pests are likely this week, and what prices he can expect if he sells early. For most of his life, farming was an exercise in instinct and luck. Now it is closer to a calculation.

In Dhaka, a small business owner opens a dashboard that shows payroll, inventory, tax filings and supplier payments in one place. A bank he has never visited offers him working capital based not on collateral, but on transaction history. He does not feel wealthy. But he feels visible.

At a clinic in Sunamganj, a paramedic enters a patient’s symptoms into a digital system. A doctor joins remotely. The diagnosis comes quickly. So does relief.

In Narayanganj, a garment worker updates her identity record and applies for a skills certificate on her phone. She is preparing for an overseas interview. The process once involved queues, agents and uncertainty. Now it is procedural, almost boring. Which is precisely the point. When systems work, people gain back time, dignity, and the emotional bandwidth to imagine better futures.

This is not a vision of a high-tech Bangladesh filled with futuristic gadgets. It is a vision of a more capable Bangladesh. One where everyday systems work well enough that people can focus on learning, earning, and improving their lives. Every technology required to build this future already exists. What separates countries that imagine progress from those that experience it is not innovation. It is intent.

Bangladesh is approaching a decisive moment. A young population, rising entrepreneurial energy, and rapid digital adoption are converging with a global economy increasingly shaped by artificial intelligence and automation. The question is no longer whether technology will reshape society. It is whether Bangladesh will use it to expand human capability or allow it to deepen existing gaps.

This moment of choice arrives as the country moves towards a national election. Elections do not, by themselves, solve structural challenges. But they create something rare in public life: the possibility of a fresh start. A new government will have the mandate to reset long-term development priorities and decide whether digital transformation will be treated as a peripheral initiative or the backbone of national strategy. This choice is not political. It is generational.

The most important challenge Bangladesh faces is not technological. It is human.

We have 85 million young people under the age of 25, and more than 40 million students who move through classrooms largely designed for memorisation rather than mastery. Workers possess talent that far exceeds the tools available to them. Small businesses, which form the backbone of the economy, remain constrained not by ambition but by access. Technology, when applied with purpose, does not replace people. It makes them more productive, more informed, and more competitive.

This has been true throughout history. The industrial revolution multiplied human output; it did not diminish human worth. Railways shrank distance and expanded opportunity. Electrification reshaped how cities, factories, and classrooms worked. Technology has always been an amplifier of human potential, not a rival to it. It has never been zero-sum. When used deliberately, it lifts entire economies.

Education remains the most important lever because productivity follows learning. Teachers who spend less time on paperwork spend more time teaching. Students assessed on understanding rather than recall learn more deeply. Technology is not a substitute for good teaching, but it can remove friction, personalise instruction, and allow teachers to do their best work. When used well, it accelerates learning. When misused, it distracts.

The same principle applies across sectors. Nurses make faster, safer decisions when they have timely information. Farmers reduce risk when they have access to forecasts and market data. Citizens save days when public services are digitised. Technology is leverage: it converts effort into outcomes.

But none of this is possible without one foundational input: cheap, reliable and widely accessible internet.

For Bangladesh, internet access is no longer a luxury. It is basic infrastructure for human capital development. A student without affordable data cannot learn digitally. A worker cannot upskill. A small business cannot formalise. A citizen cannot access government services. Digital literacy does not emerge from isolated training sessions. It emerges from daily use.

If Bangladesh wants a digitally capable population, it must treat internet access the way previous generations treated roads, electricity, and primary education. This requires revisiting the heavy tax burden on mobile data, encouraging long-term private investment, and expanding coverage outside major cities. The private sector already knows how to build networks. What it needs is a policy environment that rewards long-term investment rather than short-term extraction.

Cheaper internet does not simply increase usage. It changes behaviour. People experiment. They transact. They build confidence. Over time, a population becomes digitally fluent not because it was instructed to, but because it has no reason not to be online.

Bangladesh has already seen this dynamic in one area: digital payments. Mobile money transformed financial behaviour nationwide. It formalised parts of the economy, reduced leakage, and gave millions their first experience with digital transactions. But the next phase of progress requires deeper reform. True interoperability would make digital payments universal. Merchant fees could be lower. Fraud controls could be strengthened. Remittances could be integrated directly into wallets. The first decade showed what is possible. The second decade must make it accessible to all.

To unlock this next phase, Bangladesh will need to build something it does not yet fully have: a national digital public infrastructure stack.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Countries that have made the fastest digital leaps, most notably India with its Aadhaar identity system, UPI payments layer, and interoperable data networks, succeeded because the government built the rails and the private sector built the trains. Public systems created the foundation. Private companies innovated on top of it. The combination unlocked ecosystems, entrepreneurship, and economic participation at scale.

Bangladesh can do the same. A digital identity layer, a national payments and data exchange layer, and open APIs that allow innovators to build securely on top of government infrastructure would accelerate every part of the economy. It would reduce duplication, increase trust, and ensure that public goods remain public while private companies compete on service, value, and user experience.

Crucially, the goal is not to replace the private sector. It is to empower it. Bangladesh already has EdTech platforms, mobile money providers, logistics networks, fintechs, agritech tools, and health technology solutions built by local experts. What they often lack is the public infrastructure to integrate their services, move data securely with consent, and serve citizens at national scale.

Governments build the foundation. Domain experts build the future. This same logic applies particularly strongly to small and medium enterprises. Lack of SME visibility is the single biggest barrier to credit. When payments, compliance, identity, and transaction data can move through a common infrastructure stack, SMEs become legible to the financial system. Legibility reduces risk. Reduced risk attracts lending. Lending drives growth. Growth creates jobs. This is how a digital economy compounds.

But to sustain this shift, Bangladesh will need patient capital. Solving problems in education, healthcare, or labour markets is slow and uncertain, and investors commit to such work only when they trust the system around them. That trust depends on predictable regulation, transparent governance, and capital markets that function well enough for investors to enter and exit efficiently. Countries that have built deeper, better-regulated public markets often see an influx of foreign venture capital and private equity because risk can be priced sensibly and long-term bets feel viable. Without that foundation, early-stage innovation stalls, not because the ideas are weak, but because the financial architecture required to support them is too thin. Countries that underinvest here do not only lose startups. They lose problem-solvers.

Bangladesh must decide whether it wants to remain a consumer of digital solutions or become a producer of them. The outcomes will be visible in classrooms where students learn better, in clinics where care arrives faster, in fields where farmers increase yield, in businesses that grow beyond survival, and in workers who compete globally.

This is what techno-optimism should mean in Bangladesh. Not faith in machines, but confidence in people, supported by systems that work.

We cannot wait for the Bangladesh of tomorrow to emerge on its own. We have to build it. And the tools to build it are already in our hands.

Shahir Chowdhury is a CFA charterholder with over a decade of experience in financial services in London. He is the founder and CEO of Shikho, an edtech company.

Comments