A crude lesson: How war on Iran is reviving fears of another global oil meltdown

History has an uncanny way of reappearing when the world least desires it. More than half a century after the Arab-Israeli war of 1973 convulsed the global energy system, the US-Israel war on Iran has once again placed oil at the centre of geopolitics.

Brent crude surged beyond $100 a barrel amid fears that hostilities could choke off energy flows from the Persian Gulf. Prices spiked to levels never seen since the coronavirus pandemic disrupted markets in 2020.

For all latest news, follow The Daily Star's Google News channel.

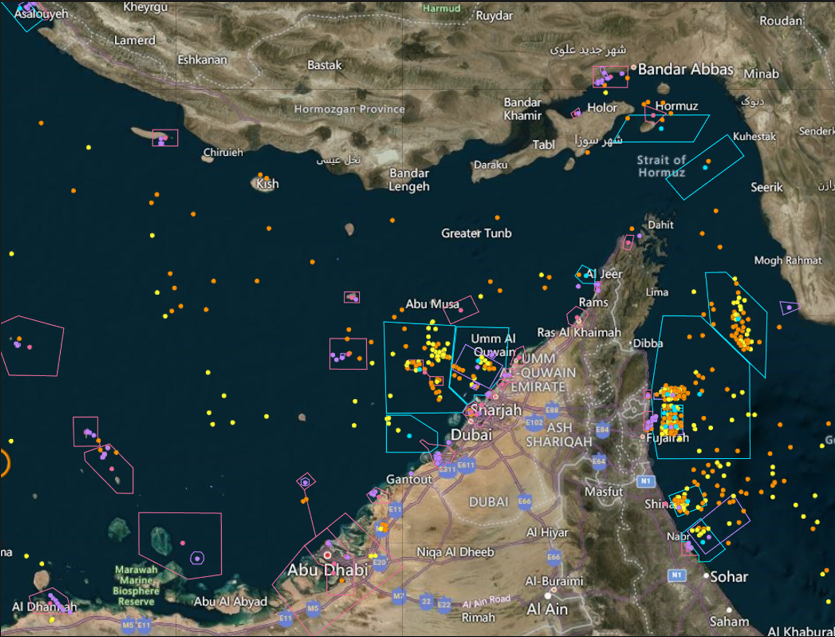

For all latest news, follow The Daily Star's Google News channel. The concern extends beyond price volatility. It centres on the risk of a systemic energy shock. The Strait of Hormuz -- the narrow maritime artery through which a vast share of the world’s oil passes -- has become a potential battlefield.

Reports from the BBC suggest Iranian forces have targeted vessels attempting to traverse the strait, forcing shipping firms to reconsider transit routes.

During the Yom Kippur War in 1973, Arab members of the Organization of Arab Petroleum Exporting Countries imposed an oil embargo on nations supporting Israel, particularly the United States and several Western allies.

Production cuts and export bans triggered a dramatic supply squeeze across industrial economies. Oil prices nearly quadrupled, rising from about $3 per barrel to roughly $12 within months.

The surge rippled through economies dependent on Middle Eastern crude. In the United States, petrol shortages became a daily ordeal as long queues formed at service stations. Governments imposed emergency measures, including lower speed limits, to reduce fuel consumption.

Western economies soon faced stagflation -- a combination of stagnant growth and soaring inflation. The crisis reshaped energy policy, pushing governments to build strategic petroleum reserves and diversify supply. The International Energy Agency itself emerged from the turmoil in 1974 to coordinate responses to supply disruptions.

Today’s crisis stems from a different dynamic. Unlike 1973, when oil producers deliberately weaponised supply through an embargo, the current turmoil arises from physical disruption caused by war.

The attack on Iran has pushed the Strait of Hormuz into strategic danger. The passage linking the Persian Gulf to the Arabian Sea carries roughly a fifth of global oil supply and a similar share of liquefied natural gas shipments.

If the corridor closes, the consequences would ripple through global energy markets.

Energy economist Bruce Kasman of JPMorgan warned, in comments reported by Reuters, that prices could reach $120 a barrel if the conflict persists. Such levels would put immediate pressure on global growth and consumer prices.

Even temporary disruptions carry serious implications. More than 90 percent of global transport still depends on oil -- from aircraft fuel to container shipping.

When oil tightens, the entire economic bloodstream constricts.

Oil remains embedded in the cost structure of nearly everything people consume. Transport, plastics, heating and electricity generation all rely directly or indirectly on petroleum or natural gas.

Reuters notes that prolonged disruptions could shave about 0.6 percentage points off global economic growth while pushing consumer prices higher. In the worst scenario, economists warn of renewed stagflation.

Asia would be particularly exposed. Countries such as India, South Korea and Japan rely heavily on Gulf energy supplies.

Natural gas markets may prove even more vulnerable, as global LNG capacity has less spare supply than oil markets.

If the crisis of 1973 reshaped global energy policy, the turmoil of 2026 may accelerate another transformation already underway.

The earlier shock pushed nations to diversify supply, build reserves and improve efficiency. Today’s disruption could speed up the shift towards renewable energy and electrification.

Yet the geopolitical geography of oil has changed little. The Persian Gulf still supplies a critical share of the world’s energy, and the Strait of Hormuz remains a narrow hinge on which global commerce can pivot or collapse.

Two power plant shutdowns triggered load shedding: Energy minister

Titas consumers to face low gas pressure until June 25

Domestic fuel prices may fall if global rates ease: Energy minister

Nepal to export 40MW power to Bangladesh

Rooppur Nuclear Plant test operations paused over technical glitch

Rooppur Nuclear Plant unit-1 to add 300 MW to national grid by August: Minister

IAEA team begins Rooppur inspection as plant enters operational phase

Russia’s Rosatom suggests floating nuclear power unit for Bangladesh

Padma Bridge Service Area-2 power bill down from Tk 5.21 lakh to Tk 75,714