Appointment row leaves Islami Bank dry in just two weeks

In just fourteen days, Islami Bank Bangladesh PLC has moved from a stable liquidity position into a severe cash crunch, following disruption around the appointment of its new chairman by the Bangladesh Bank.

In the face of mounting withdrawal pressure, the central bank yesterday dissolved the bank’s entire board and appointed an administrator. But much of the liquidity damage had already been done.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The country’s largest private-sector bank, which had begun to recover under the interim government after years of massive loan irregularities and financial misconduct linked to the S Alam Group, is now under renewed liquidity pressure as deposit outflows accelerate.

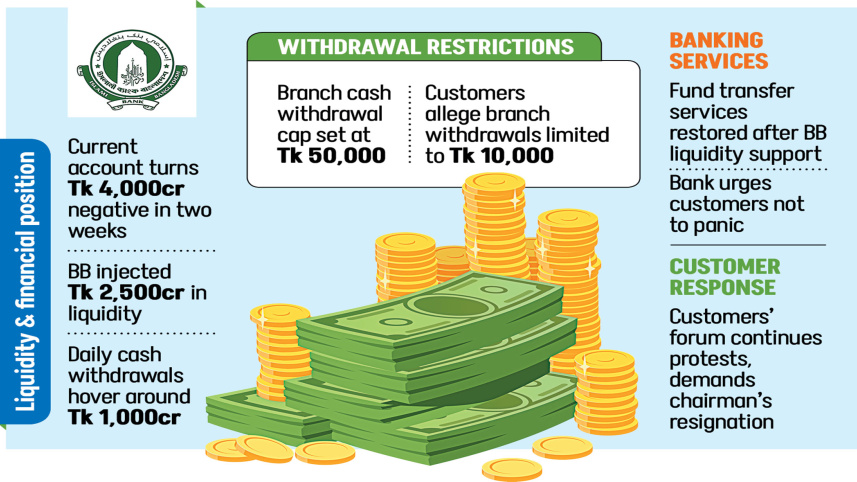

The bank’s current account with the central bank was in a positive position until May 31. But within the past two weeks, it has moved into a deficit of about Tk 4,000 crore, show data.

A current account with the central bank is a master reserve account held by commercial banks and financial institutions. It acts as the clearing mechanism for interbank transactions and allows institutions to settle daily obligations.

When the balance falls into deficit, banks can face difficulties in fund transfers and clearing operations, which can disrupt services for customers.

Md Altaf Hossain, managing director (current charge), acknowledged the pressure. He told The Daily Star yesterday that the deficit had widened due to the bank’s reliance on liquidity support from the central bank.

Hossain said fund transfer services and other clearing operations resumed after the bank received liquidity assistance from the banking regulator.

The acting managing director also said customers are withdrawing around Tk 1,000 crore a day on average. Deposits are coming in at a similar level, but the scale of withdrawals is putting pressure on the bank.

As a result, the bank has imposed a Tk 50,000 cash withdrawal limit per customer at the branch level, he added.

However, some customers said branches in Dhaka were allowing withdrawals of only Tk 10,000 amid the ongoing pressure.

The Bangladesh Bank yesterday injected Tk 2,500 crore in special liquidity support to help the country’s largest shariah-based lender address the acute cash shortage. Bangladesh Bank Executive Director and Spokesperson Arief Hossain Khan confirmed the development to The Daily Star.

The bank has also failed to maintain the required cash reserve ratio (CRR) with the central bank and has faced difficulty paying depositors due to heavy withdrawal pressure since the start of the month.

According to internal data, Islami Bank’s total deposits fell from Tk 1,84,382 crore on May 31 to Tk 1,80,141 crore on June 7. Facing the pressure, the lender sought Tk 10,000 crore in liquidity assistance from the Bangladesh Bank last week.

On June 12, the central bank Governor Mostaqur Rahman hinted at possible support for the bank at a post-budget press conference.

“The crisis at Islami Bank will be resolved soon. Depositors will not face difficulties in withdrawing their money. If necessary, emergency liquidity support will be provided,” said the governor.

On Sunday, Islami Bank’s management met the Bangladesh Bank governor to discuss the situation.

After the meeting, Md Altaf Hossain told journalists that discussions focused on business and liquidity management following the central bank’s emergency support.

He said the newly received funds would be used based on identified needs, including withdrawal patterns, sectoral requirements and projected liquidity needs in the coming days.

He added that Bangladesh Bank’s expert team would review and verify the bank’s data.

HOW INSTABILITY UNFOLDED

On May 24, just as the country was preparing for a week-long Eid holiday, the Bangladesh Bank appointed Md Khurshid Alam, a former deputy governor, as chairman of Islami Bank hours after the previous chairman resigned.

The appointment came as a surprise and triggered immediate concern among stakeholders.

After the Eid holidays, on June 1, a group under the banner of the Conscious Customers’ Forum began protests outside the Islami Bank head office at Motijheel in Dhaka.

On the first working day after the holidays, hundreds gathered there demanding that the Bangladesh Bank cancel the appointment and reinstate former Islami Bank managing director Omar Faruk Khan.

Khurshid was among four senior Bangladesh Bank officials who resigned amid protests by central bank employees shortly after the fall of the Awami League government on August 5, 2024.

The Conscious Customers’ Forum continued its demonstrations, calling for the resignation of the new chairman.

Jamaat-e-Islami’s visible support for the protests, along with statements from senior leaders, suggested strong opposition to the appointment.

The government and opposition have also exchanged allegations over Islami Bank’s role in recent years, including during the last general election.

The home minister told the House that the bank had favoured Jamaat, while Jamaat MPs rejected the claim and demanded the remarks be removed from the record.

The Islamist party is widely believed to have maintained close links with Islami Bank since its establishment in 1983.

FINANCIAL HEALTH OF THE BANK

Islami Bank currently holds the largest volume of non-performing loans (NPLs) in the banking sector, amounting to Tk 95,629 crore, or 50.88 percent of its total loans.

The bank was taken over by controversial conglomerate S Alam Group in 2017. The group later channelled around 80 percent of the bank’s loans to its own companies and affiliated firms, according to allegations widely documented in the banking sector.

After the fall of the Awami League government in a mass uprising, the bank was freed from the group’s control and is now operating under a board of independent directors appointed under the Bangladesh Bank oversight.

“A large share of the defaulted loans is linked to the S Alam Group, and recovery remains minimal,” the bank’s Acting Managing Director Altaf said.

He added that the bank is trying to recover loans from other borrowers as well, but progress has been slow as even regular customers have become reluctant to repay.

Comments