A dangerous turn in banking reform

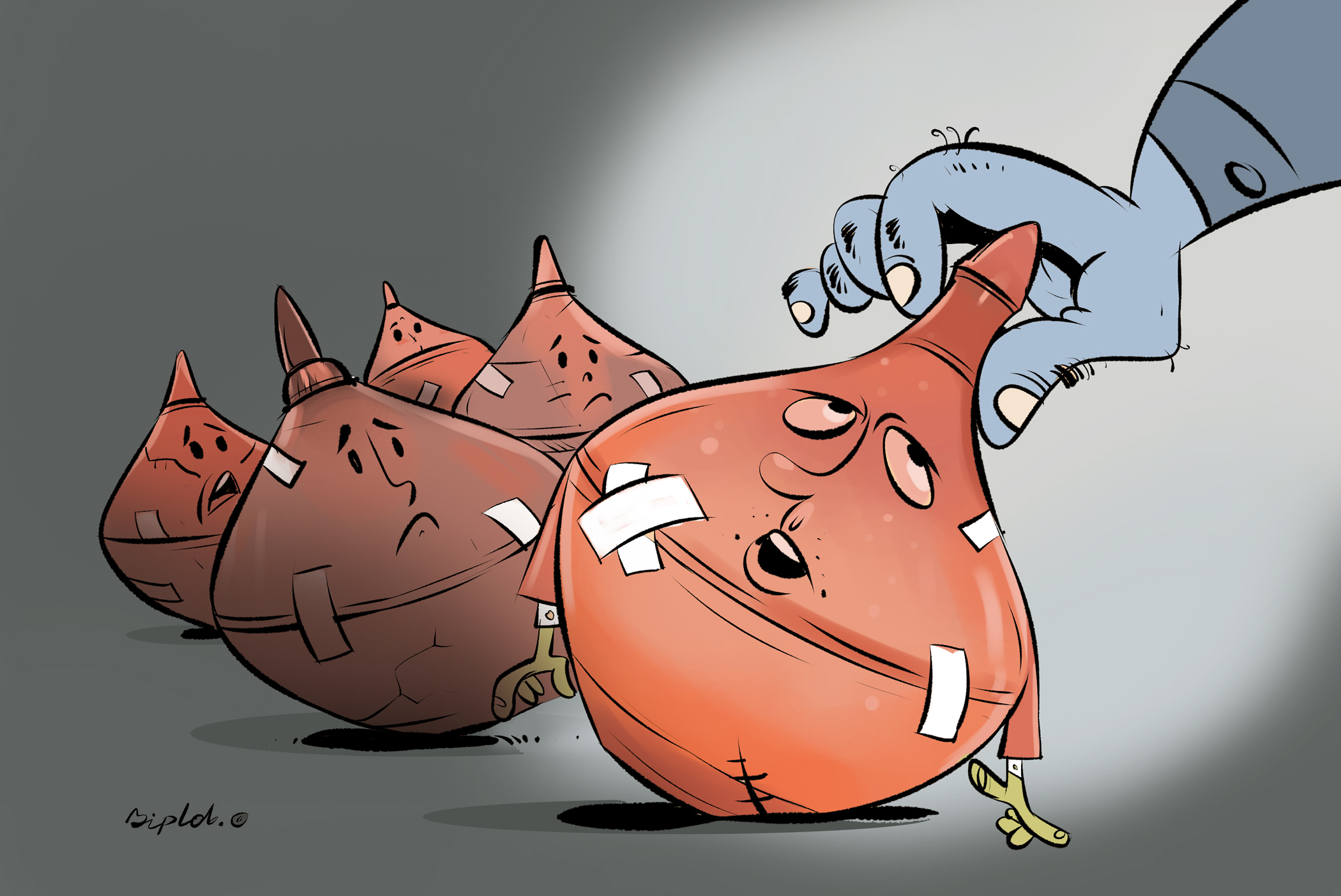

Reform, in Bangladesh, has a short shelf life. Not long after the interim government began cleaning up the country’s rotten banking sector, the BNP administration walked back much of the work. A new law now lets the former owners of five scandal-plagued Shariah banks buy their way back in. The price? A mere 7.5 percent upfront of whatever the state pumped in to keep the institutions alive.

The government and Bangladesh Bank together injected Tk 35,000 crore into what became “Sommilito Islami Bank”, a state-run vehicle created to absorb the wreckage of First Security Islami Bank, Social Islami Bank, Union Bank, Global Islami Bank, and Exim Bank. Under the Bank Resolution Act 2026, former owners can reclaim the lot for Tk 2,625 crore -- with the rest repayable over two years at a gentle 10 percent simple interest. It is, as one economist drily noted, a reward rather than a reckoning. The amount is also meagre compared to what these very owners allegedly siphoned out through years of rule-bending.

The five banks were not victims of misfortune. They were victims of their owners. Four were dominated by S Alam Group, whose chairman, Mohammed Saiful Alam, stands accused of using depositors’ money as a personal treasury. The fifth, Exim Bank, was long the fiefdom of Nassa Group’s Md Nazrul Islam Mazumder. Between them, these men presided over years of related-party lending, regulatory evasion, and outright embezzlement. Public deposits were treated as private vaults. Millions of ordinary savers are still waiting to recover their money—and may wait years longer.

The original ordinance, passed in May 2025, barred these owners from any involvement. The interim government had been making genuine headway: restructuring boards, initiating mergers, signalling that the old order was finished. Confidence in the sector, badly battered under Sheikh Hasina’s rule, had cautiously begun to return. Many savers were starting to trust the banks again. The new law puts that recovery at risk. Bangladesh Bank officials now warn, with some understatement, that if former owners return, taking the banks back a second time will not be easy.

Zahid Hussain, former lead economist at the World Bank’s Dhaka office, puts it plainly. Allowing wrongdoers back in “reinforces a culture of impunity.” It tells the financial sector that the consequences of looting are negotiable. It tells depositors that the state’s promises are, too. After so many reforms, audits, and a formal merger process, he warns, reversing everything through a single legal adjustment raises serious doubts about whether institutional reform in Bangladesh can ever stick.

Birupaksha Paul, a professor of economics at the State University of New York in Cortland, goes further. The new act, he argues, is a “pernicious compromise” for the BNP government -- one that will “further deteriorate the banking health of the economy mainly because of its implied moral hazards.”

The concern is not just about these five banks. It is about what the law signals to every banker, every borrower, and every regulator in the country: that recklessness has a price, and it is negotiable. The government, Birupaksha warns, is “going against the grain of social and moral expectations which wanted to see a new banking order.”

The new law is not without guardrails, to be fair. Applicants must inject fresh capital, settle creditor claims, and submit to two years of close monitoring. Bangladesh Bank must conduct due diligence and seek government clearance before any transfer. On paper, the safeguards look reasonable. In practice, Bangladesh’s banking regulators have not historically been known for their steeliness when facing well-connected businessmen. The same governance failures that produced this crisis are bound to come back.

There is a pattern worth noting. The Awami League once passed a power purchase law ostensibly designed to attract private investment and fix an energy shortage. It ended up benefiting a narrow group of well-connected businessmen at the public’s expense. The law was widely seen as a template for how policy in Bangladesh gets shaped -- not around national interest, but around the interests of those with access. The Bank Resolution Act, passed quietly on a Friday, fits the same mould.

Which raises the uncomfortable question that the amendment’s critics are now asking openly: is the BNP government simply caving to pressure from powerful business groups? Is the word “oligarch” -- once used almost exclusively to describe the Hasina era -- making an unwelcome return? Bangladesh is not the first country to discover that banking reform is politically uncomfortable. Oligarchs, by definition, have resources and connections. They push back. Governments, facing other pressures, find reasons to accommodate them. The technical language of resolution frameworks provides convenient cover.

What is harder to explain away is the timing and the optics. A government serious about reform does not sell banks back to the people who broke them. It does not do so while depositors wait in line.

The government insists it is cleaning up the mess left by the Awami League. On the evidence of the new law, it is at least partly recycling it.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Comments