Banks’ provision shortfall surges

The provision base of the banks in Bangladesh deteriorated further in the second quarter of 2021 because of the surging bad loans, highlighting the worsening health of the financial industry.

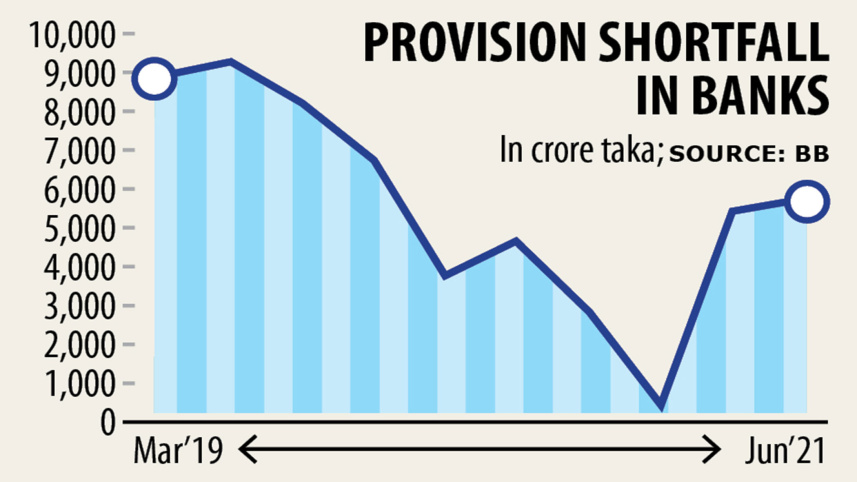

The shortfall stood at Tk 5,583 crore at the end of the March to June period, up a staggering 40 times from December last year and 7 per cent from three months earlier, data from the Bangladesh Bank showed.

The deficit was up 24 per cent year-on-year.

A provision shortfall occurs when a financial obligation exceeds the amount of cash available.

It can be temporary, arising from a unique set of circumstances, or persistent, indicating poor financial management practices.

Banks have to set aside 0.50 per cent to 5 per cent of their operating profit as a provision against general category loans, 20 per cent against classified loans of substandard category, and 50 per cent against classified loans of doubtful category.

It has to keep aside 100 per cent against classified loans of bad or loss category.

The provision situation may erode further as default loans could escalate in the coming days since there is no sign of improvement from the ongoing business slowdown.

Between March and June, the shortfall widened due to the lacklustre performance of 11 banks, which faced a combined deficit of Tk 14,858 crore.

The banks are Agrani, BASIC, Janata, Rupali, Bangladesh Commerce, Dhaka, Mutual Trust, National, Social Islami, Standard, and Bangladesh Krishi Bank.

Some of the banks have been facing a shortfall for years due to a lack of corporate governance.

The shortfall of the state-run banks stood at Tk 10,727 crore, which resulted from a wide range of financial scams. Janata Bank alone had a shortfall of Tk 5,351 crore.

Among the private lenders, National Bank witnessed the highest level of the shortfall, amounting to Tk 2,394 crore in June in contrast to a deficit of Tk 435 crore six months ago.

The provisioning shortfall narrowed throughout 2020 after borrowers were granted wholesale moratorium support from the central bank due to the economic hardship caused by the coronavirus pandemic.

The payment holiday had barred banks from downgrading the credit status of borrowers even if they failed to pay instalments regularly.

As a result, defaulted loans did not increase on paper, allowing banks to earmark a lower amount of the operating profit to cover bad loans.

The central bank withdrew the moratorium largely in December last year, pushing up both the non-performing loans (NPLs) and the provision shortfall.

NPLs stood at Tk 99,205 crore in June, up 11.80 per cent from six months earlier and 3.21 per cent year-on-year.

Salehuddin Ahmed, a former governor of the central bank, said that the escalation of the provision shortfall indicated that the financial health of the banking sector had deteriorated.

"The shortfall has also tainted the image of the banking sector. Both local and global investors are losing their confidence in the banking sector."

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. For instance, weak banks can't open letters of credit (LCs) directly with their counterparts in other countries.

First, they have to secure an additional guarantee, known as "add confirmation", from other banks having a global presence.

So, local banks have to pay a hefty amount in charges and commissions to the confirming banks, adversely impacting the LC issuing banks, Ahmed said.

"Banks should lend cautiously to avoid NPLs. This will reduce the requirement of provisioning."

Comments