Regulatory ‘time tax’ holding back investment, says World Bank

The World Bank (WB) has described regulatory burdens in Bangladesh as a tax on time and investment, saying they are holding back investment compared with peer economies.

“Complex, fragmented, and discretionary regulatory processes impose a substantial time tax on firms in Bangladesh, with clear consequences for investment and growth,” said the WB in its latest Bangladesh Development Update.

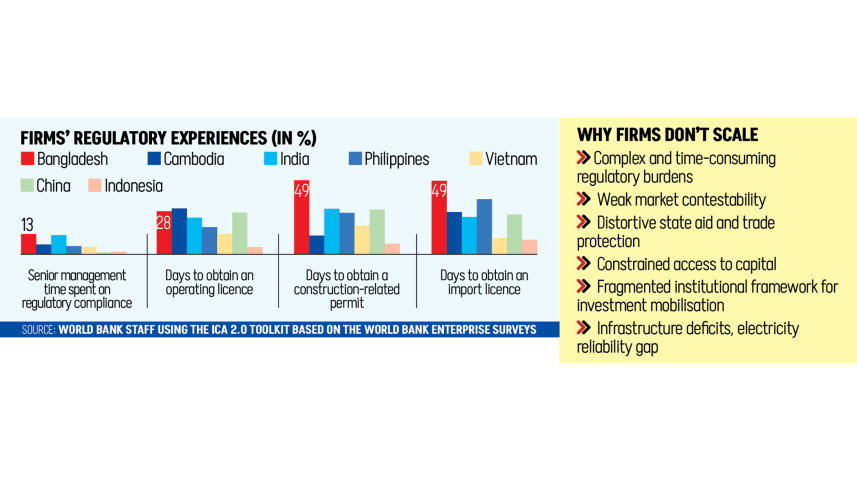

According to the WB report, senior managers spend an average of 13 percent of their time dealing with government requirements, more than in any comparable country in the region.

The headline figure, however, conceals far heavier pressures in parts of the country.

In Chattogram, managers devote about 40 percent of their time to regulatory compliance. In Barishal, the share rises to 60 percent, leaving little room for productive management and strategic decision-making.

The burden also falls unevenly.

Frontier firms, defined as the most productive companies in the formal sector, spend around five percentage points less time dealing with regulators and face fewer tax inspections than non-frontier firms.

Regulatory delays compound these challenges. Securing an operating licence takes 28 days on average. Construction permits and import licences take about 49 days each, nearly twice as long as in China or India, according to the report.

Starting a formal business in Bangladesh is also costly. At roughly $10,000, the price of entry exceeds 10 percent of annual revenue for more than half of firms younger than six years.

The consequences are tangible. Firms facing heavier regulatory demands are 19 percent less likely to invest.

That weakens competition, slows the shift of resources to more productive companies and entrenches productivity gaps across the private sector, according to the WB.

“Improving the business environment is central to sustaining growth and absorbing a rapidly expanding workforce,” said Dhruv Sharma, senior economist and lead author of the report.

“Reducing regulatory uncertainty, offering targeted deregulation, strengthening competition, and easing constraints to firm growth will help unlock private investment and jobs,” he added.

Revenue per worker in manufacturing and services stands at roughly one-third of the South Asian average. In services, the largest employer, labour productivity has stagnated since 2016.

POLICY BIAS TOWARDS FRONTIER FIRMS

The report said that policy support has tended to favour a small group of high-performing frontier firms.

Preferential tax treatment, subsidised finance and trade privileges have flowed disproportionately to them, while most small and medium-sized enterprises and high-potential informal firms operate in a far less supportive environment.

Tax policy offers a clear example. The standard corporate income tax rate is 27.5 percent, but readymade garment and textile manufacturers enjoy preferential rates of 12 percent to 15 percent, largely granted through discretionary Statutory Regulatory Orders (SROs), according to the report.

Such exemptions led to foregone corporate tax revenue equivalent to 2.4 percent of GDP in 2021 alone, a sizeable cost in a country where the tax-to-GDP ratio hovers around 8 percent.

Access to finance deepens the divide. State-backed credit schemes have offered exporters loans at rates as low as 2 percent, while other producers pay up to 13 percent.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The Export Development Fund (EDF), a central bank initiative providing low-cost foreign currency financing to exporters for raw material procurement, reached $9.29 billion in the 2020 to 2021 fiscal year.

As a result, 42 percent of frontier firms report having a bank loan or line of credit, compared with 29 percent of non-frontier firms. The disparity widens their ability to invest and expand.

The WB report said trade policy adds another layer.

The bonded warehouse scheme, which allows duty-free imports of inputs, remains more than 90 percent concentrated in the readymade garment sector and related industries, despite repeated pledges to extend it to others.

Meanwhile, firms serving the domestic market face average import duties of about 10.9 percent on final goods, roughly double the South Asian average. The result is a structural anti-export bias that makes protected domestic production more lucrative than competing abroad.

Finance constraints continue to curb upgrading. Around 22 percent of firms are partially credit-constrained and 8 percent fully constrained. Companies with bank loans record labour productivity about 4.5 percent higher than those without, underlining the role of finance in adopting technology, expanding capacity and investing in skills, according to the report.

It said strict collateral rules, limited credit scoring for young firms and weak insolvency frameworks further restrict the flow of capital to its most productive uses.

DUALITY IN REGULATORY POLICIES

The country’s private sector has developed a stark dual structure shaped by trade, industrial and regulatory policies.

According to the WB, high tariffs and para-tariffs, discretionary rules and selective incentives have favoured larger, established and export-oriented companies.

A small group of highly productive frontier firms now operates alongside a much larger pool of non-frontier firms, including small and medium-sized enterprises and informal businesses with growth potential.

Frontier firms, defined as the top decile of formal companies by productivity, are on average 11 times more productive than non-frontier firms and have continued to pull further ahead.

This divide creates a sharp imbalance between output, exports and employment. Frontier firms generate three-quarters of total sales but account for just 15 percent of formal jobs.

By contrast, most employment growth has come from non-frontier firms, particularly in domestically oriented services and younger, smaller manufacturers.

Yet these businesses face weaker incentives and tighter constraints when they seek to invest, formalise or scale up, said the report.

The gap between revenues and jobs is even starker in the RMG sector. Frontier firms in the sector generate almost half of national revenue but provide only one in 12 formal private sector jobs.

Broadening opportunities beyond this narrow group is therefore critical to creating more and better-paid work, according to WB.

It said that Bangladesh’s investment promotion is also fragmented.

Over the past two decades, responsibilities for investor outreach, registration, incentives, land development, licensing and aftercare have been split among multiple bodies, including Bangladesh Investment Development Authority, Bangladesh Economic Zones Authority and Bangladesh Hi-Tech Park Authority, as well as line ministries and some subnational authorities.

Overlapping mandates, weak coordination and the absence of a single body accountable for results have become structural obstacles to diversification, according to the report.

ELECTRICITY RELIABILITY GAP

Unreliable electricity supply is the most frequently cited obstacle to doing business in Bangladesh. Power disruptions have repeatedly interrupted production and eroded output for firms.

Compared with peers in South Asia, firms in Bangladesh wait longer for electricity connections and endure more frequent outages, averaging 26 a month.

For the median firm, outages wipe out nearly 9 percent of annual sales. About a quarter of companies resort to generators at times, driving up costs.

Weak grid reliability, particularly outside major economic hubs, widens regional disparities and undermines competitiveness.

With demand for electricity expected to grow by about 7 percent a year to 2030, the WB said reforms will be needed to improve efficiency and ensure the financial sustainability of power generation and distribution.

FIRMS CHOOSE TO STAY INFORMAL, BUT WHY

Informality remains widespread in Bangladesh because many businesses see little incentive to register.

Many stay outside the formal system not for lack of information, but because they judge that engagement with tax and regulatory authorities does not deliver benefits commensurate with the risks and costs of greater visibility.

Around 40 percent of informal enterprises already operate at productivity levels similar to small formal firms, despite limited access to formal markets, bank credit, supplier development schemes or government support.

Informality, the report said, reflects institutional and policy constraints rather than weak productivity.

SETTING PRIORITIES FOR REFORM

The WB called for a phased reform plan to tackle distortions across the economy while supporting firm upgrading and diversification.

The first step is broad reform to reduce uncertainty, lower business costs, strengthen competition, address informality and mobilise private capital.

Next come trade reforms to reduce barriers. Finally, market and sector measures should target priority segments such as small and medium-sized enterprises with strong job creation potential.

The WB said that a cross-cutting principle underpinning the reform matrix is the move toward a smart deregulation approach.

That means easing compliance for low-risk activities while tightening enforcement where risks are higher, simplifying cumbersome rules, introducing risk-based licensing and inspections, and expanding digital procedures.

Comments