How robust is the balance of payments?

There is considerable hype on social media about a big turnaround in the balance of payments (BoP) under the interim government. As evidence, numbers with varying degrees of accuracy are cited on the build-up of foreign reserves and the associated reduction in the current account deficit. The objective of this essay is to explain recent developments in the BoP, assess the robustness of the adjustment process, and suggest policy options for moving forward.

The underlying causes of the BoP crisis are long-standing and deep-rooted. The immediate triggers were a series of external shocks relating to Covid-19, the global inflation of 2021-2022, and the Russia-Ukraine war that began on February 24, 2022. These shocks lowered global GDP growth and trade, while raising global commodity prices, inflation and interest rates. Their adverse effects on the BoP of Bangladesh were magnified by poor macroeconomic management, reflected in a fixed exchange rate, artificially low interest rates, large fiscal deficits driven by the Covid-19 response, and excessive use of bank credit to finance these deficits.

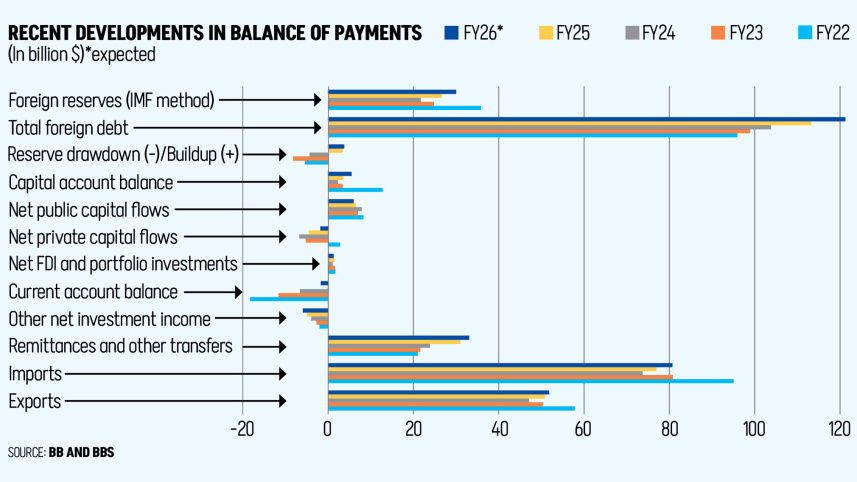

As a result, export earnings fell, the cost of imports surged, the volume of trade financing declined, and its cost increased. The net outcome for the BoP was a huge surge in the current account deficit, which reached a record $18.2 billion in FY2022. This sharp increase put pressure on reserves.

The government was initially slow to respond and chose to absorb the shock through reserves. The rapid rundown of reserves soon made clear that this was not sustainable. Bangladesh, therefore, entered a three-year IMF adjustment programme in January 2023. Although policy adjustments began then, most progress occurred between May 2024 and June 2025. Interest rates were deregulated, the exchange rate was unified and made market-based, fiscal deficits were reduced mainly through cuts in public development spending, and bank financing of fiscal deficits was curtailed.

Export earnings recovered in FY2025, remittance income surged, and imports fell sharply. The current account deficit narrowed to a small level in FY2025. The exchange rate stabilised at a realistic level consistent with market behaviour. With strong public capital inflows, Bangladesh reversed the reserve drawdown and recorded a notable balance of payments surplus in FY2025.

How robust is this stability? Can it be sustained as GDP growth and investment recover under a newly elected democratic government?

First, export earnings in FY2025 were still about $7 billion lower than in FY2022. Moreover, in the first eight months of FY2026, exports fell by 3 percent, raising concerns about the outlook for the BoP. On the positive side, the sharp acceleration in remittance earnings, which were $9 billion higher in FY2025 than in FY2022, has been a lifeline.

Second, and most significantly, the value of imports fell by $19.5 billion between FY2022 and FY2025. This decline largely explains the improvement in the current account deficit of $18.1 billion over the same period.

Third, reserves rose modestly by $5 billion in FY2025 and by a further $5 billion in January 2026. However, they are projected to decline during the second half of FY2026 because of weaker exports and a pickup in imports. Overall, barring any major policy setback or a prolonged Iran war, reserves are expected to stabilise at around $30 billion.

What is often missing in media commentary is recognition that, alongside the reserve build-up, total external borrowing has surged from $103.8 billion in FY2024 to $113.2 billion in FY2025 and is projected to reach $122.8 billion by the end of FY2026. The increase in external debt of $19 billion between FY2024 and FY2026 would far exceed the modest rise in reserves of $7.2 billion.

The fall in imports was initially driven by quantitative restrictions. Although these have been relaxed in recent months, a combination of higher interest rates, depreciation of the real effective exchange rate, improved terms of trade due to lower global commodity prices, and a sharp slowdown in GDP growth has reduced the nominal value of imports in US dollars.

GDP growth slowed to 3.5 percent in FY2025. Negative export growth in the first eight months of FY2026, rising external debt and debt servicing, and the onset of the Iran war raise doubts about the durability of the present BoP situation. Much of the growth slowdown reflects a weaker investment climate, including deterioration in law and order, political uncertainty during the transition to an elected government, energy constraints, cuts in ADP spending, high trade logistics costs, anti-export bias in trade policy, and skills shortages.

With the smooth conduct of a national election and transfer of power to an elected government, the growth outlook has improved. But much will depend on how quickly the new government implements a comprehensive set of reforms on multiple fronts. Importantly, a recovery in economic growth will bring a sharp increase in imports, while higher global energy prices linked to the Iran war will also raise import costs.

Research by Policy Research Institute (PRI) shows that, over the medium to long term, the income elasticity of imports in Bangladesh is around one. This is broadly consistent with findings for India, Sri Lanka, Pakistan, Indonesia and Vietnam. A recovery in GDP growth will therefore require sufficient BoP space for imports to expand along the long-term trend.

Illustrative projections for FY2025-FY2030 show that if GDP growth rises to 7 percent by FY2030, with inflation falling to 5 percent and the real effective exchange rate remaining stable, imports would need to grow by an average of 10.8 percent per year between FY2025-FY2030. Assuming a sustainable current account deficit of around 1 percent of GDP, combined earnings from exports and remittances would need to grow by about 10.1 percent annually to maintain BoP stability.

What are the policy implications? Alongside policies to reduce inflation to 5 percent, the most fundamental challenge is export diversification. The recent surge in remittances largely reflects a shift of transactions from hundi to formal channels. Over time, remittance growth is likely to stabilise at around 5-6 percent per year. Exports will therefore need to grow in double digits to finance imports linked to stronger GDP growth.

RMG will remain dominant, but double-digit export growth will not be possible without diversification. PRI research shows that this requires reforms in several critical areas. One key requirement is flexible exchange rate management that avoids appreciation of the real effective exchange rate. A fixed nominal rate and sharply appreciating REER between FY2011 and FY2023 proved highly damaging for exports and the BoP. This must be avoided.

A second priority is the removal of the anti-export bias in trade policy. PRI research provides empirical evidence of how this bias has constrained the expansion of non-RMG exports. The recent correction in exchange rate management is welcome and is already benefiting exports and remittances. However, it must be complemented by lower trade protection that currently harms non-RMG exports.

Other priorities include improving the investment climate by addressing constraints in energy, trade logistics, infrastructure and skills. Participation in global value chains, export-oriented foreign direct investment, free trade agreements and greater investment in research and development will also help expand the non-RMG export base.

Policies are also needed to improve the quality of the capital account. The surplus in FY2025 was driven largely by public external borrowing, including exceptional BoP financing from the IMF and other multilateral partners. This was necessary but is clearly a short-term measure. Sustained reserve accumulation will depend on careful management of the current account and a stronger, more diversified export base.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Finally, a sustainable external capital mobilisation strategy is essential. Multilateral medium and long-term financing will remain important. However, debt servicing, particularly amortisation, is rising as access to concessional financing declines and commercial borrowing becomes more prominent. Sustained inflows of foreign direct investment and continued access to trade credit at reasonable cost will therefore be crucial. Strengthening the investment climate and creditworthiness of Bangladesh will help attract these flows.

The writer is vice chairperson of the Policy Research Institute of Bangladesh (PRI). He can be reached at sadiqahmed1952@gmail.com

Comments