BB holds policy rate at 10% in tough trade-off: inflation vs growth

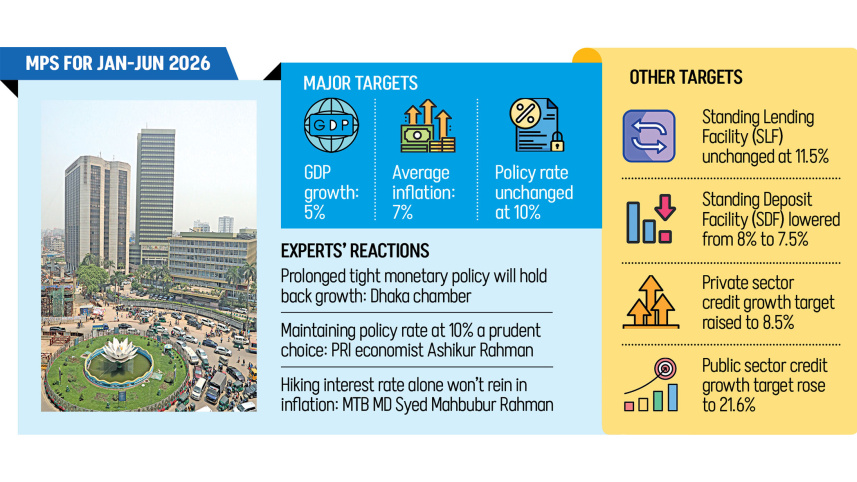

The Bangladesh Bank (BB) kept its policy rate unchanged at 10 percent yesterday, citing persistent high inflation ahead of the national election this week.

The policy rate, or repo rate, is a key tool used to influence credit demand and money circulation, aiming to contain demand-driven inflation. The central bank said it would maintain its tight monetary stance throughout the January-to-June period.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. In line with this approach, the BB has kept the double-digit policy rate since October 2024.

Despite this monetary tightening, inflation rose for the third consecutive month, reaching 8.58 percent in January.

Rising food prices ahead of Ramadan, the month of fasting for Muslims when demand for certain food items usually ticks up, contributed to the increase, according to the state statistical agency BBS.

The 12-month average inflation in January stood at 8.66 percent, well above the BB’s target of reducing the price pressure below 7 percent.

While unveiling the monetary policy, BB Governor Ahsan H Mansur said many objectives had been achieved, but inflation remained above target. He highlighted broader economic improvements, especially in governance and stabilising the banking and financial sector.

“However, inflation remains slightly behind target. The goal was to bring it down to around 7 percent, but it is still about 8.5 percent,” Mansur said, adding that monetary policy alone cannot achieve all outcomes, and that it must be coordinated with fiscal measures.

In the Monetary Policy Statement, the BB reduced the Standing Deposit Facility (SDF) rate, at which commercial banks park excess liquidity with the central bank, by 50 basis points to 7.5 percent.

Amid weak private-sector credit growth, the adjustment is intended to discourage banks from holding funds at the BB and encourage lending to the private sector.

Credit to the private sector fell to a historic low of 6.1 percent in December, while public-sector lending rose to 28.9 percent. However, the projection for private-sector credit growth was at 7.2 percent and public-sector growth at 20.5 percent.

Mansur noted that government borrowing heavily influences the money market, tightening liquidity and keeping interest rates high, which crowds out private-sector lending.

“Total credit has grown, but a large portion has gone to the government rather than the private sector, creating distribution pressure,” he said.

In the Monetary Policy Statement, the BB projects public-sector credit growth to reach 21.6 percent in the second half of FY26, driven by pre-election fiscal spending and post-election administrative expenditures during the government transition.

Besides, the government’s budget target of borrowing Tk 1,18,000 crore from the banking system was factored into this projection.

The governor said domestic credit expansion is strong, but private-sector lending could have grown faster if government borrowing were lower.

Mansur said persistent government demand in the money market keeps pressure on overall demand and prevents interest rates from falling rapidly.

He said high rates, though restrictive, have helped stabilise the exchange rate and supported foreign reserve accumulation.

“Earlier, Bangladesh repeatedly failed to meet IMF reserve targets, but since August 2024 all quarterly targets have been achieved or even exceeded, even before receiving IMF funds,” Mansur said.

Gross foreign exchange reserves stood at $34.06 billion yesterday, up from around $26 billion a year earlier. Under IMF calculations, reserves were $29.47 billion according to the BPM6 model.

The policy statement noted that economic activity remained broadly stable, supporting a positive growth outlook. “However, political developments, soft industrial output, persistent inflation, and global headwinds may undermine growth prospects,” it added.

Inflation has moderated, but at a slow pace, suggesting expectations are not yet firmly anchored around the target. “This development underscores the need for continued policy tightening, which should cool inflation further by the end of this fiscal year,” the statement said.

Syed Mahbubur Rahman, managing director of Mutual Trust Bank, told The Daily Star that the policy rate alone cannot curb inflationary pressure, given supply-chain constraints and other factors.

He said that most loans in Bangladesh are corporate, with only 10 percent in retail, so interest rate hikes do not affect consumers immediately. Private-sector loan demand would not rise sharply even after the election.

Birupaksha Paul, professor of economics at the State University of New York in Cortland, said the 10 percent repo rate remains appropriate but is contributing to cost-push inflation.

“Private credit growth was 6.1 percent in December 2025 and is projected to be 8.5 percent in June 2026. While that part is tightened with the aim of reducing inflation, public-sector credit growth, projected at 21.6 percent, will be the main driver of sustained high inflation.”

He noted that the projection is ambitious, given that public-sector credit reached 28.9 percent in December 2025. Additional spending on new pay scales could make reducing it to around 22 percent difficult.

Paul, a former chief economist of BB, added that the economy may gain momentum after the election, but its strength will depend on improvements in law and order.

Ashikur Rahman, principal economist at the Policy Research Institute, said the BB’s cautious stance is justified as inflation remains stubbornly high. The recent rise in prices appears partly driven by electoral dynamics, which boost consumption ahead of national elections.

Fahmida Khatun, executive director at the Centre for Policy Dialogue (CPD), said contractionary monetary policy is appropriate given persistent inflation, but fiscal policy also needs tightening, and market monitoring should be strengthened.

She added that a prolonged tight stance is unfavourable for investment, but controlling inflation must take priority.

In a reaction, the Dhaka Chamber of Commerce and Industry expressed concern over the BB’s decision to maintain a contractionary stance solely to control inflation.

“The reality, however, tells a different story. Despite prolonged tight monetary conditions, inflation has not been effectively contained, proving that this tool has largely failed while inflicting serious damage on productive economic activities,” the chamber said.

Comments