BB sticks to tight monetary policy as inflation stays high

Every monetary policy comes with trade-offs. And the Monetary Policy Statement (MPS) the Bangladesh Bank unveiled yesterday is no exception.

One of its biggest dilemmas is that the central bank is trying to cool stubbornly high inflation while simultaneously injecting money into the economy through several channels.

For all latest news, follow The Daily Star's Google News channel.

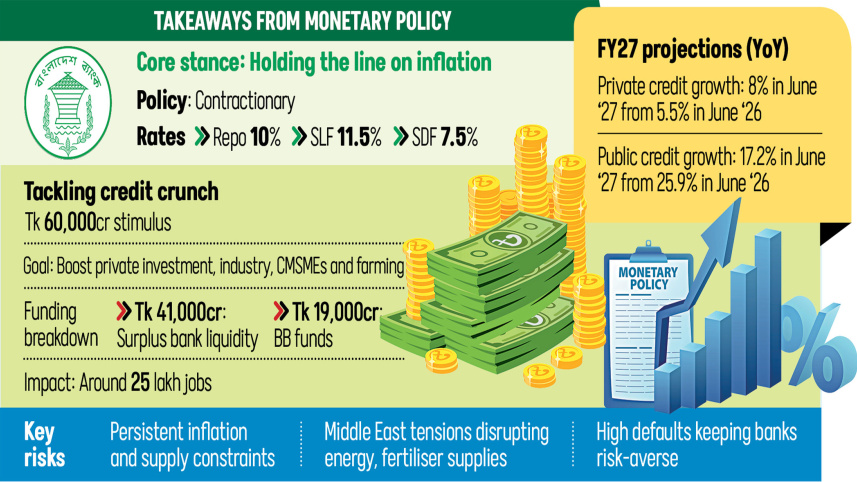

For all latest news, follow The Daily Star's Google News channel. Identifying near double-digit inflation as its biggest challenge, the BB kept the policy rate, its benchmark lending rate, unchanged at 10 percent for the July-December period.

The policy rate, also known as the overnight repurchase rate, is the rate at which commercial banks borrow from the central bank. It has remained at 10 percent since October 2024 after 11 consecutive increases between May 2022 and October 2024.

The Standing Lending Facility (SLF) rate will remain at 11.5 percent, while the Standing Deposit Facility (SDF) rate will stay at 7.5 percent.

Despite the BB maintaining a contractionary monetary policy for years, inflation has remained above 9 percent. It stood at 9.42 percent in May, the highest level in 16 months and well above the central bank’s 7.5 percent target for fiscal year 2026-27.

Economists say the impact of high interest rates has been diluted by BB’s continued liquidity support to weak banks and its purchases of US dollars from the market. Together, these measures have softened the effect of tighter monetary policy.

Over the years, the central bank has injected more than Tk 75,903 crore in emergency liquidity support into troubled conventional and Islamic banks.

Recently, it has announced a Tk 60,000 crore stimulus package for industries affected by the economic slowdown, including support to reopen closed factories. The package is designed to channel credit to productive sectors rather than flood the broader economy with cash.

The BB says the package will not fuel inflation because Tk 41,000 crore will come from surplus liquidity already available in the banking system rather than from new money creation.

INFLATION CANNOT BE BEATEN BY INTEREST RATES ALONE

One of the clearest acknowledgements in the MPS is that tighter monetary policy alone cannot curb inflation driven by structural weaknesses, supply chain bottlenecks and market inefficiencies.

Besides, energy supply-side shocks from the Middle East conflict have exacerbated inflationary pressures. Investment remains sluggish, and overall economic activity shows signs of stagnation.

Speaking at the policy announcement at BB headquarters, Deputy Governor Habibur Rahman said market management would play a crucial role in bringing inflation under control.

Governor Md Mostaqur Rahman unveiled the policy, his first since taking office in February.

The deputy governor said bringing inflation down would require support from other policymakers and agencies, adding that inflation had eased from its earlier peak, suggesting monetary policy had not been ineffective.

“Ensuring discipline in the market and preventing unnecessary hoarding, syndication and price manipulation are essential. At the same time, the Bangladesh Bank remains ready to use all available monetary policy tools,” he added.

BALANCING INFLATION AND GROWTH

The new monetary policy attempts to strike a balance between containing inflation and reviving economic growth.

The central bank said its primary objective remains maintaining low and stable inflation, while price stability is essential for sustainable growth and investment.

In the monetary policy, the BB projects GDP growth of 6.1 percent in FY27, below the government’s target of 6.5 percent.

The MPS also highlights an unusual feature of the economy. Many banks are sitting on ample liquidity, yet demand for private sector loans remains weak. The reasons include high financing costs and banks wary of rising defaults amid a surge in non-performing loans.

Still, the central bank expects private sector credit growth to reach 6.8 percent by December. In April, it stood at just 4.75 percent, the second-lowest level in more than a decade.

Reserve money, or base money created directly by the central bank, rose from negative 0.1 percent in June last year to 9.2 percent by the end of FY26. The BB projects reserve money growth of 7.5 percent by December, even as it continues to inject liquidity into the financial system.

Public sector credit growth is projected at 21.8 percent by December after reaching an estimated 25.9 percent in June.

Mustafa K. Mujeri, executive director of the Institute for Inclusive Finance and Development (InM), said the BB’s primary responsibility is to control inflation. However, in a developing economy like Bangladesh, it must also support growth.

“Since inflation has remained persistently high for the past three years, the central bank has little choice but to maintain a contractionary monetary policy,” he said.

ECONOMISTS CALL FOR STRONGER FISCAL SUPPORT

According to Mujeri, the fact that inflation has not declined over the last three years indicates that it is not being driven solely by excess demand.

“There are other contributing factors. Therefore, simply keeping the policy rate high will not be enough.”

The economist said monetary policy alone cannot curb inflation and stressed the need for coordinated fiscal policy, stronger market management and effective supply-side measures. Those complementary policies, however, have been implemented poorly, allowing inflation to remain elevated.

He added that high borrowing costs are only one reason investment remains weak. The bigger constraints are the energy crisis, particularly gas shortages, along with extortion and other structural bottlenecks. Without addressing those issues, lowering interest rates alone will do little to revive investment.

Fahmida Khatun, executive director at Centre for policy dialogue (CPD), said policymakers face the difficult task of containing inflation while reviving investment and growth.

With inflation remaining high for about four years, there is little room for an expansionary monetary policy, making the decision to keep the policy rate unchanged justified, she said.

“While liquidity support for industries could aid recovery, it may weaken monetary tightening unless directed toward productive investment, employment and productivity.”

She said stronger public investment, exports, remittances and structural reforms could support growth. However, if private investment and credit remain weak, achieving the government’s GDP growth target will be difficult.

Economist Abu Ahmed criticised the policy mix, saying liquidity injections and higher government borrowing from banks contradict a tight monetary stance.

He argued that high interest rates discourage genuine entrepreneurs, while inflation is being driven by multiple factors, and called for lower lending rates to encourage investment, employment and growth.

Syed Mahbubur Rahman, managing director of Mutual Trust Bank, said higher interest rates are less effective in Bangladesh than in advanced economies.

“Limited banking penetration, reliance on informal credit, supply-driven inflation and a business-focused banking sector mean higher interest rates mainly discourage investment rather than significantly reducing consumer demand,” he added.

Ashikur Rahman, principal economist at the Policy Research Institute of Bangladesh (PRI), said the MPS rightly identifies supply chain inefficiencies, energy prices, exchange rate movements, fertiliser costs and global geopolitical shocks as key drivers of inflation.

“Even so, monetary policy cannot afford ambiguity. When inflation expectations remain elevated, the central bank must clearly signal that price stability is its overriding priority,” Ashikur added.

Comments