Banks no longer making most of their money from lending

businesses, as weak lending threatens investment and growth

In 2021, banks earned most of their income the traditional way -- by lending. Four years later, lending, the core business of banking, became a relatively minor source of earnings, according to their financial reports.

As private sector credit growth slowed and non-performing loans (NPLs) mounted, net interest income of banks came under increasing pressure. At the same time, sluggish imports also weighed on commission income from trade-related services such as opening letters of credit (LCs).

To survive and, for many, to thrive, commercial banks, whose DNA is to create credit and take calculated risks by backing businesses, instead took shelter in the safety of Treasury bills, lured by their higher returns.

On paper, banks now appear highly profitable because of those elevated Treasury yields. They are earning strong returns without taking credit risk.

But economists and bankers say the windfall comes with two risks.

If banks continue to favour government securities over lending, private investment could weaken further, slowing the country’s economic recovery. And if Treasury yields begin to fall, banks will simply fail to maintain their current level of earnings.

INCOME PATTERN SHIFTS SWIFTLY

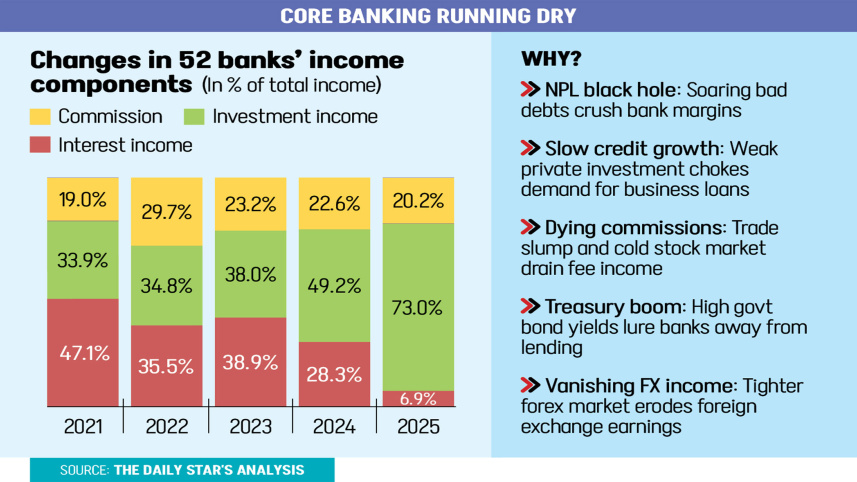

In 2021, the country’s 52 major banks generated a combined Tk 40,793 crore in income.

Interest income accounted for 47 percent of the total, while investment income contributed 34 percent. The remaining 19 percent came from commission income, according to financial reports of the commercial lenders.

In 2022, investment income increased but remained below interest income. The overall pattern changed little in 2023.

The balance shifted swiftly in 2024, when investment income overtook interest income to become the largest source of banks’ earnings.

By 2025, net interest income accounted for just 6.8 percent of total income, while investment income surged to 73 percent. Commission income contributed around 20 percent.

Syed Mahbubur Rahman, managing director and chief executive officer of Mutual Trust Bank, said this is a matter of serious concern.

He said foreign investors have already warned that banks could face significant difficulties if Treasury bond yields start to decline.

Explaining the shift in banks’ income sources, he said the cost of deposits has risen alongside overall operating expenses, narrowing lending margins.

“The biggest issue is that NPLs [non-performing loans] in the banking sector have risen sharply. As a result, banks are not receiving interest income from a large portion of their loans, yet they still have to pay interest to depositors.”

“Consequently, net interest income has declined. Ideally, a bank’s primary source of income should be its net interest income, as lending is its core business,” he added.

The CEO said the growing volume of bad loans has handicapped banks. At the same time, credit growth has slowed, prompting commercial lenders to increase their investments in Treasury bonds.

“Commission income has also declined because the country’s trade volume has weakened. In addition, the margins that banks previously earned from foreign exchange transactions have largely disappeared.”

“For the long-term sustainability of banks, their core income remains critically important. However, given the current state of private sector investment, sluggish credit growth, and the fact that NPLs have yet to improve,” he said, adding, “I do not expect the situation to improve in the near future.”

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. CONCERNS OVER INVESTMENT, GROWTH

Another notable trend is the steady decline in banks’ net interest income over the past three years. Commission income also fell by around 8 percent year-on-year in 2025.

Investment income, however, has risen gradually over the past five years.

Kazi Monirul Islam, chief executive officer of Shanta Asset Management, said banks had a clear incentive to invest in Treasury securities because they offered attractive yields while lending became significantly riskier.

“That is why investment income has increased,” he said.

Monirul said banks naturally gravitate towards areas where they can earn higher returns with lower risk.

However, when banks choose government securities over extending loans, the wider economy suffers. If the trend continues, it will constrain private investment and slow the country’s economic recovery, he added.

As long as Treasury yields remain high, banks are likely to continue posting strong earnings. Once yields begin to fall, banks may initially benefit from capital gains on their Treasury portfolios, said the CEO of the asset management firm.

“Over time, however, their overall income is also likely to decline,” he added.

He believes that unless economic growth strengthens, banks will struggle to redirect the large volume of funds currently invested in government securities into productive private sector lending.

On the decline in commission income, Monirul said subdued imports and weaker export earnings had reduced trade-related fees and commissions.

Banks that operate brokerage houses also earned less commission because of weak trading activity in the stock market. However, he expects commission income to improve this year.

According to data from the Dhaka Stock Exchange (DSE), average daily turnover stood at Tk 1,474 crore in 2021. It fell to Tk 960 crore in 2022 and Tk 578 crore in 2023.

Turnover declined further to Tk 566 crore in 2024 before plunging to Tk 51 crore in 2025.

Comments